Florida. The dream. Palm trees swaying in a warm Gulf breeze, mornings so golden they look filtered, and zero state income tax to sweeten the whole deal. I packed my entire life into a moving truck and headed south with a vision that felt earned after decades of work. It took less than two years for that vision to completely unravel.

Once considered the ideal place to live out one’s golden years, Florida is quickly losing favor with retirement-aged folks. I am living proof of that shift. What follows is the honest, sometimes uncomfortable, sometimes infuriating story of why I left. No sugarcoating. No regrets about the decision to go.

Let’s dive in.

1. Housing Prices Exploded and Took My Budget With Them

Let’s be real: Florida used to be affordable. That story is completely over now. In just half a decade, the median price of a single-family house in Florida rose roughly sixty percent. That is not a gentle market correction. That is a wrecking ball aimed directly at fixed-income retirees.

According to Redfin, the average cost of a home in March 2018 was approximately $250,000. By July 2024, the median sale price had climbed to $409,700. I had budgeted for a retirement, not a bidding war. Even those who already owned their homes felt the ripple: rising costs for maintenance, HOA fees, and utilities can slowly chip away at your fixed income, month after quiet month.

Remote workers and the wealthy are flocking to the state and driving up home prices, leaving those on a fixed income feeling the pinch. When the people moving in next door are thirty-five-year-old tech employees on full remote salaries, the neighborhood economics shift fast. And retirees on Social Security are the ones left scrambling.

Over the ten years ending in 2024, housing costs increased by 132 percent in Florida, the second-largest spike among states. That number still stops me cold. No retirement plan I had ever seen accounted for anything remotely close to that kind of surge.

2. Home Insurance Became a Monthly Financial Crisis

Honestly, nothing blindsided me more than the insurance situation. I knew it would cost something. I had no idea it would cost this much. Florida residents had the highest home insurance rates in 2024, and although things are stabilizing in 2025–2026, costs are still very high. Data from Insurify found that the average annual home insurance premium nationally was $3,259 in 2024, while Florida came in at more than four times that amount at $14,140.

In the past three years alone, home insurance premiums in central Florida grew by forty percent. As of October 2025, the average home insurance premium in Florida is around $8,800 annually, with some providers charging upwards of $12,000 to $15,000. Think about that in relation to a monthly Social Security check. The math is brutal.

More than twenty insurers have stopped writing new homeowners policies in Florida or pulled out of the market entirely. That means fewer choices, weaker competition, and zero incentive for prices to drop. Roughly seven out of ten Florida homeowners experienced rising insurance costs or coverage changes, such as their insurer dropping them, according to a 2024 Redfin survey. Seven out of ten. That is not a fringe problem. That is the norm.

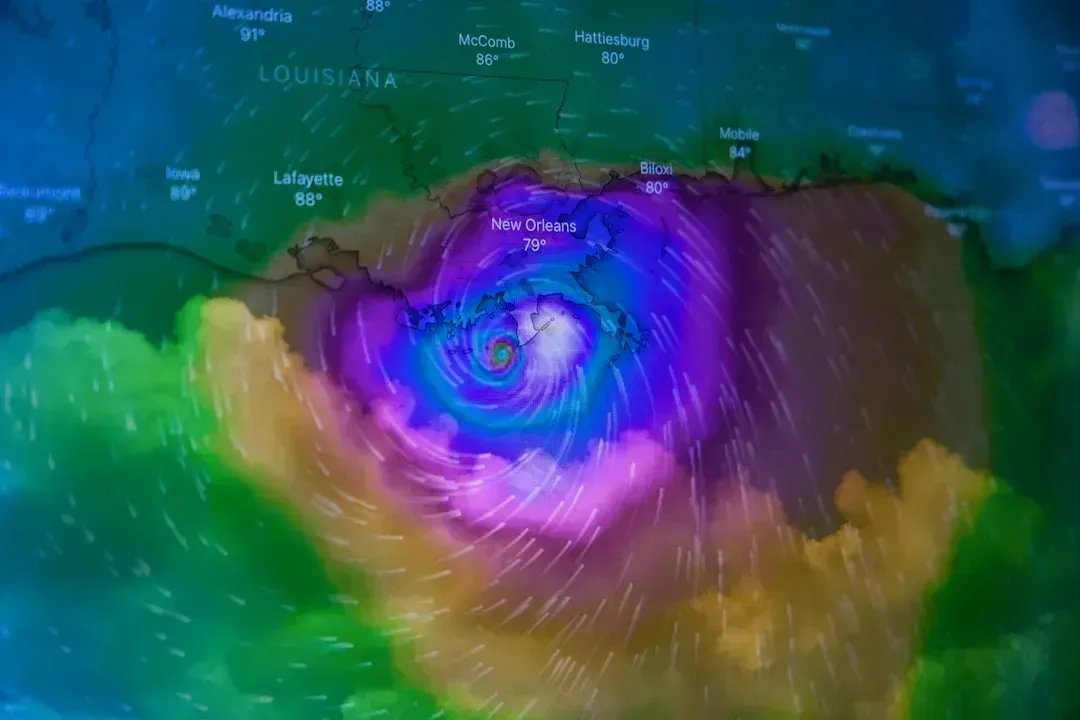

3. Hurricane Season Was Not a Season. It Was a Lifestyle.

I knew about hurricanes. Everyone does. What I did not understand was what it actually feels like to live under that constant shadow for months at a time. Most Floridians have to have a go-bag ready for last-minute evacuations and be prepared to leave behind what they cannot fit in their car. This is not an emergency preparedness tip. This is a way of life.

In September 2024, Hurricane Helene hammered Florida and the Southeast, killing more than 230 people, making it the deadliest hurricane to strike the U.S. since Hurricane Maria ravaged Puerto Rico in 2017. Some estimates put the economic impact of Helene, including property and infrastructure damage, as high as $200 billion.

The National Centers for Environmental Information reported that the state was hit with 94 disaster events between 1980 and 2024. That includes floods, wildfires, winter storms, freezings, droughts, severe storms, and hurricanes or cyclones. Put another way, Florida receives around two natural disasters annually, placing retirees and their property at significant risk.

Power outages, evacuations, damaged homes, and flooded streets are no longer rare events. They are becoming part of the regular conversation. I came to Florida to rest, not to spend six months a year scanning weather radar apps in a low-grade panic.

4. The Traffic Congestion Stole Hours From Every Single Day

Here is the thing about Florida traffic: it does not get better. It compounds. Florida is the third most populous state, with between 300,000 and 380,000 new residents arriving each year. Every one of those people needs to be somewhere, and somehow they all seem to need to be there at the same time as you.

In 2024, Tampa drivers lost 34 hours to congestion, costing the city $800 million. Miami fared worse, with drivers wasting 74 hours annually at a cost of $1,325 each, totaling $3.4 billion in lost productivity statewide. Seventy-four hours a year. Nearly two full work weeks, just sitting in traffic. In retirement.

The Fort Myers-Cape Coral metro area ranks as the 13th worst in the country for traffic congestion, with residents losing approximately 48 hours each year stuck in traffic. I moved to Florida for peace and quiet. I got gridlock and exhaust fumes instead. The irony of spending your “relaxing retirement” white-knuckling a steering wheel on a Florida interstate is not lost on me.

5. The Heat and Humidity Were Genuinely Relentless

Two summers in, I understood why people miss actual seasons. There is a kind of psychological wear that comes from endless heat that no one prepares you for. Everyone knows that Florida is warm and humid, but people are often still surprised by how oppressive the weather can be. Retreating indoors does not always bring relief, because air conditioning is drying and is often difficult to regulate.

Many retirees do not realize how much they will miss experiencing winter, spring, and fall until they find themselves in endless summer and decide to move back north to enjoy the four seasons. It sounds trivial until you live it. Missing the crunch of autumn leaves or the quiet magic of the first snowfall turns out to be a real grief, not a small one.

Florida’s heat is not just inconvenient, it is a genuine health consideration for older adults. Think of it like running a car engine in the red zone all summer, every summer, with no cooldown. For seniors with cardiovascular conditions or respiratory issues, sustained extreme heat is not just uncomfortable. It is dangerous.

6. The Healthcare System Was a Shocking Disappointment

You would assume a state where more than one in four residents is aged sixty-five or older would have a world-class healthcare system. You would be wrong. A 2025 WalletHub study ranked Florida at number 42 in the entire country, firmly among the bottom ten worst healthcare systems nationwide.

Rapid population growth is straining Florida’s healthcare systems and essential public services. Hospitals and clinics see higher patient volumes and longer wait times. For a retiree who depends on regular specialist visits or chronic condition management, “longer wait times” is not a minor inconvenience. It is the difference between managed health and a medical crisis.

Long-term care in Florida, which Medicare tends not to cover, can reach anywhere from $63,000 to over $130,000 per year, depending on how much attention is required, according to 2024 data from Genworth. That is a number that can quietly erase a lifetime of savings in just a few years. I spent my retirement driving hours to medical appointments I should have been able to book locally. That wears you down fast.

7. HOA Fees and Rules Were Suffocating

Nobody tells you about the HOAs until you are already living inside one. Florida hosts approximately 50,100 HOAs, the second highest in the nation. About sixty-four percent of property owners deal with these associations, and monthly fees average $230, adding roughly $2,760 to annual housing costs before any special assessments hit.

In addition to mortgage payments, many retirees face homeowners association fees, particularly in Florida’s numerous gated communities and retirement developments. HOA fees in 2025 average between $400 to $600 per month in luxury or resort-style communities. In some buildings, maintenance fees for 2024 jumped by as much as fifty percent between special assessments and increased insurance costs. That is a serious monthly drain on a retirement budget that was never designed to absorb it.

Miami-Dade County’s median monthly condo association fee jumped over fifty-nine percent from 2019 to 2024, while in Broward fees leaped more than fifty-six percent to $613. The rules that come attached to those fees are their own story. What color you can paint your front door, whether you can park your own vehicle in your own driveway. It is not retirement. It is managed living.

8. The “Tax-Free” Promise Was Only Half the Story

The no-state-income-tax selling point is real. I am not going to pretend it isn’t. However, I think that single fact has been used to paper over a much more complicated tax reality. Do not confuse “no state income tax” with “no taxes at all.” State and local taxes in Florida can take a serious bite out of your retirement savings. The combined state and local sales tax averages 7.00% in Florida, according to the Tax Foundation.

Property taxes surged roughly sixty percent over the past five years, rising alongside skyrocketing home values in popular retirement areas. The state also charges a six percent sales tax on most purchases, with some local areas pushing this higher. These taxes affect daily expenses from groceries to restaurant meals, creating a higher cost of living than many retirees anticipate.

Grocery prices in Florida experienced a notable increase, with a 4.3% rise between March 2024 and March 2025. When insurance, property taxes, and groceries all climb simultaneously, that income tax break starts to feel like a single umbrella in a category-four storm. A single retiree can expect to pay an average of $73,646 a year to live comfortably in Florida, which means you would need at least a $2.2 million nest egg to sustain that over thirty years.

9. Overcrowding Turned Paradise Into a Pressure Cooker

The Florida I imagined was quiet mornings, uncrowded beaches, and slow easy days. The Florida I found was packed with people at every turn, in every season. Florida is the third most populous state, with between 300,000 and 380,000 new residents arriving each year, and its aging infrastructure is scrambling to keep up.

Florida’s rapid population growth has resulted in increased traffic congestion, overdevelopment, and a loss of the serene environment many retirees seek. The proliferation of strip malls and high-density housing has altered the state’s landscape, diminishing its appeal. The beaches I moved there for? Packed. The restaurants I looked forward to? Forty-five-minute waits on a Tuesday.

The seasonal population increase between November and April, commonly known as snowbird season, can drive up prices on everything from groceries and gas to restaurant reservations and recreational activities. Crowded services and longer wait times may also lead some retirees to seek out more exclusive and more expensive options just to maintain their comfort during peak months. There is no winning that game on a fixed income.

10. The Sense of Community I Expected Was Never There

I think this might be the quietest reason on this list, and maybe the most important. I moved to Florida expecting to find a community of people in similar life stages, a place where neighbors knew each other and slowed down together. Instead I found a state in constant motion, a revolving door of snowbirds, tourists, new transplants, and remote workers. It never stopped moving long enough to feel like home.

The PODS Moving Trends Report from 2025 showed that the push of people moving to Florida is lessening. From 2021 to 2023, Florida had six or more cities in the top ten most moved-to cities, whereas in 2024, only two Florida cities made the list, while two others were among the most commonly moved-out-of cities. That tells you something. The dream has a growing asterisk next to it.

Data from the U.S. Census Bureau backs up the findings, showing a steady decline in the number of 65-plus Americans moving to Florida since 2020. Some retirees are heading to states like Tennessee, North Carolina, or areas of the Midwest that offer a lower cost of living, more predictable weather, and less crowding. Georgia was the most popular destination for people leaving Florida, accounting for more than ten percent of outbound migration in 2024, with Texas coming in second at a similar share. I followed that trail north myself, and I have never once regretted it.

Final Thought

Florida is a genuinely beautiful place. I am not here to trash it entirely. The sunsets are real. The winters, when they exist, are gentle. However, the version of Florida that was sold to my generation of retirees has been quietly replaced by something harder, louder, more expensive, and far less predictable than the brochure ever let on.

According to a 2024 survey of American retirees between the ages of 62 and 75 by the Employee Benefit Research Institute, 31% said their spending is much higher or a little higher than they can afford, up from 27% in 2022 and 17% in 2020. Those numbers are not abstract. Those are real people watching their savings dissolve in real time, in a state that promised them ease.

Retirement is supposed to be freedom. If the place you choose to spend it costs you your peace of mind every single month, it might be worth asking yourself: is the sunshine worth it? What would you have chosen, knowing what you know now?

Leave a Reply